July 18, 2026

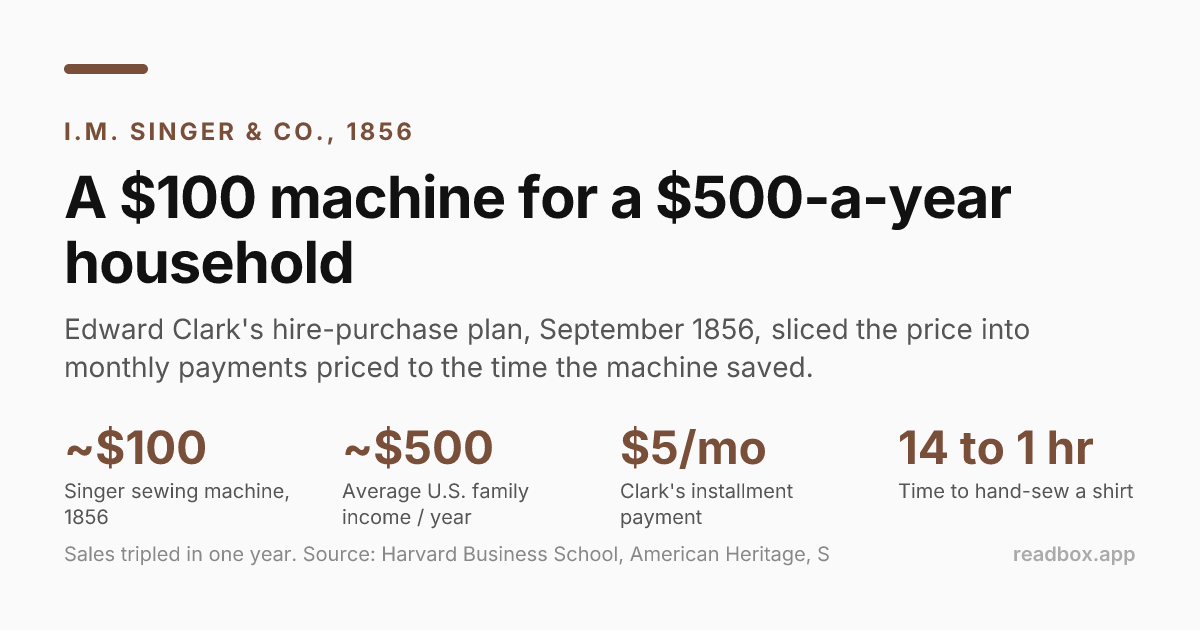

A Singer Cost $100 When a Family Made $500. His Lawyer Invented Installments, and Buyers Preferred $100 in $5-a-Month Payments to $50 Cash.

Subscribe

In 1851 Isaac Singer built a better sewing machine in eleven days. It was useless as a product until his lawyer, Edward Clark, figured out how to sell a $100 machine to households earning $500 a year, by slicing the price into monthly payments priced to the time the machine saved.

On August 12, 1851, Isaac Merritt Singer patented the first practical sewing machine. He had not invented the device; Elias Howe held the lockstitch patent and was suing everyone who tried to sell one. Singer was a flamboyant failed actor and mechanic who had taken a machine in for repair in a Boston shop and, eleven days later, produced a better one. He was, by his own account, indifferent to the invention. "I don't care a damn for the invention," he said. "The dimes are what I'm after." His lawyer, Edward C. Clark, took three-eighths of the patent in lieu of legal fees the penniless inventor could not pay, and quietly built the business.

The business had a problem. Singer's machine cost about $100 to $125, and the average American family earned around $500 a year. A sewing machine was a quarter of a household's annual income. The industrial market was small, because factories already had a cheap power source: working-class women, for whom sewing was one of the few respectable jobs. The household market, where the machine could pay for itself, was locked behind the price.

Two deals in 1856 unlocked it. First the legal one. Singer, Wheeler & Wilson, and Grover & Baker had been burning their profits suing one another. In Albany that year they formed the Sewing Machine Combination, the first American patent pool, bringing in Howe on a $5-per-machine royalty. The litigation tax fell away, and Singer was free to manufacture at scale.

Then the demand one. In September 1856, Clark introduced the hire-purchase plan: a family could take a machine home for a small down payment and pay it off in monthly installments of $5, owning it when the balance cleared. It was the first installment plan sold on a national scale by a major American company. Clark had borrowed the cue from New York furniture makers and New England clockmakers, but the sewing machine was the product that turned consumer credit into a mass market.

The mechanism was not charity. A sewing machine was a capital good that paid for itself in time. It cut the labor to make a shirt from fourteen hours to one. The installment plan matched the payment schedule to the savings the machine produced, so $5 a month was less than the value of the hours it gave back. The price had not changed; the cash-flow timing had.

Clark built the rest of the demand machine around it. In February 1856 he offered a $50 trade-in credit for any "inferior or wholly worthless" machine, meaning anything that was not a Singer, and the company destroyed the trade-ins to kill the second-hand market. He sold machines to ministers' wives at half price so a chorus of pious women would vouch that the device was respectable rather than unladylike. He replaced independent agents who also peddled rivals' models with exclusive Singer demonstrators, hired women to run the machines in public to disprove the belief that women could not operate machinery, and opened hundreds of branch offices, one of the earliest national retail chains.

The strangest sign that the plan was doing something beyond affordability came from Scientific American, which noted in the 1850s a fact that baffled its writer:

A woman would rather pay $100 for a machine in monthly installments of five dollars than $50 outright, although able to do so.

The installment plan was not merely helping people afford the machine. It was lowering the pain of parting with the money at all.

It worked. Sales tripled in a year. Manufacturing cost ran as low as $23 for a machine priced at $110, and as mass production pushed the price down the ladder, from $125 toward $10, volume exploded. By 1880 Singer produced more than 500,000 machines a year. By the time Singer died in 1875 the company was turning a profit of $22 million a year, and it had become one of the first American multinationals, selling across Europe and into Russia through its own retail network. It never skipped a dividend.

The takeaway. Singer did not win on the machine, which was neither the first nor, by most accounts, the best. He won because Clark found the real binding constraint, and it was not the price. It was the timing mismatch between a cost charged all at once and a benefit that arrived in daily saved hours. The installment plan closed that gap by pricing the payments to the cash flow the asset itself generated, so a household never had to lay out money it could feel. The trade-in-and-destroy trick, the clergy discount, the demo agents, and the retail chain were the same instinct applied to every other friction standing between a good product and a mass market. A modern operator should steal the core move: when a product pays for itself over time but will not sell at a lump sum, do not cut the price. Cut the payment into pieces smaller than the benefit the buyer receives each month, and let the asset finance its own purchase.

Want the next one?

Every new Business History Daily issue by email. One tap to unsubscribe.